Equity Markets

2024 was another strong year for investors, with US markets advancing 25.0% and international markets up 5.5%. Key themes of the year include Artificial Intelligence (AI), political news, and Federal Reserve/ monetary policy.

Artificial Intelligence (AI)

Despite advancing in the background for many years, AI has been a main investment theme and an engine for growth at almost every turn for the last 1.5 years. Heavy business spending and a growing track record of applicable use cases have demonstrated that AI can actually deliver a substantial productivity boost.

Political news:

The election of Donald Trump and Republican majorities in Congress have pushed the market to factor in (to an ever-changing extent) increased tariffs, decreased regulation for American businesses, and a stable tax environment.

Federal Reserve & monetary policy:

Stock and bond markets perpetually attempt to predict the path of interest rates with accompanying effects on security prices. From May until September, it appeared that inflation was falling away, and the path to lowering rates was clear. This outlook shifted in October when inflation readings showed stickiness, and both Presidential candidates displayed no desire to address persistent federal spending deficits. However, the underlying question remains the same as it always does… What’s next? Here are a few important considerations that frame the question:

Recent success:

Over the past two years, the S&P 500 is up 57.8%. Excluding the “Magnificent 7” stocks (the largest stocks in the index) during that same period, the return for the S&P 493 is about 32%, a strong return but far lower which reflects a market advance that is less broad than we’d like. Of the billions of dollars spent to build AI large language models, their associated infrastructure, and AI applications, the lion’s share is represented by the “Mag 7”. Because AI investment is, for now, so concentrated in a small number of companies, a stall or fall in the AI trade would likely be side-stepped by a large section of the market. For this reason, we continue seeking companies who may benefit from AI, but aren’t subject to the same capital spending requirements.

Money Supply:

Since the start of the 2020 calendar year, the S&P 500 is up 97.4%. Although a material rise in its own right, the advance pales when considering that M2 (a common proxy for the money supply) has risen 39.3% over that same time. The Federal Government’s response to the Covid-19 pandemic released an unprecedented amount of money to the American consumer (roughly $4 Trillion). The stock market both 1) reflects the consumption habits of these check recipients and 2) is the investment avenue of choice for savers. As such, it is not all that surprising that most of that money would find itself pushing up share prices.

Economic Indicators:

The unemployment rate (currently at 4.2%) remains at relatively historic lows that many officials consider healthy. Consumer sentiment remains strong as changes in real GDP and Personal Consumption Expenditures (PCE) indicate that the consumer is happy to spend (especially on services). A population that is both largely employed and willing to spend is a strong foundation for economic growth and further stock price appreciation.

Valuation:

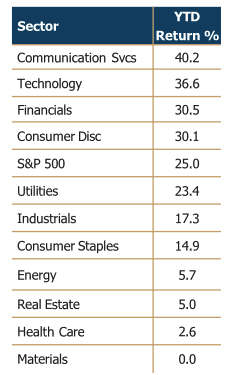

The difference between growth and value stocks, in terms of valuation, remains intact, though perhaps even more pronounced than usual. Growth areas of the market are those exposed to AI, such as the information technology and consumer discretionary sectors. Expectations here are high, and investors will be more sensitive than normal to the earnings season releases that report bottom-line results and the forward guidance of company management.

Value areas such as the healthcare, consumer staples, energy, materials, and utilities sectors are more attractively priced having retreated in December 2024. There is a comparatively lower bar in this segment of the market.

We will continue to monitor the development of these trends and find opportunities to invest in quality companies at reasonable prices.

Fixed Income Markets

On September 18, 2024, when the Federal Reserve first lowered overnight interest rates, they did so in an eye-catching fashion, reducing by 0.50%. “Recalibration” became the new buzzword, a term offered up to reflect a move away from a rigid focus on inflation towards a broader effort to shore up the labor market. That it took place on the cusp of an incredibly divisive election cycle didn’t go unnoticed.

Through a re-calibration, the Federal Reserve also projected interest rate cuts through 2026 totaling 2.5%. In the press conference that followed, Jerome Powell, Chairman of the Federal Reserve, went to great lengths to state that the Fed was pleased with the progress made on inflation. In its judgment, inflation was on a sustainable path back to the 2% target. Under the new policy pacing, the Fed followed up with two more 0.25% cuts in early November and mid-December, cumulatively lowering rates by 1.0% in 2024.

Barely three months later, inflation and unemployment met expectations, and the economy grew at 2.5 – 3.0%. The only input that appears to have shifted is a new political landscape. Yet, the Fed is dialing back the re-calibration in ways, and for reasons, that are not yet clear. The December forecast shows higher inflation next year and expected interest rate cuts through 2026 totaling only 2.0%.

Usually, when the Fed lowers the overnight rate, longer rates follow. This time, however, while the Fed lowered the overnight rate throughout the quarter, the bond market went in the opposite direction and pushed long rates higher. We see at least three reasons the response is overdone.

Current inflation is at target

As measured by the Personal Consumption Expenditures Index (PCE), the Fed’s preferred measure, inflation reached 2.1% in September 2024, just a hair above its 2.0% target. The Fed could claim credit for achieving its target from a high of 7.5% in 2022. Job well done. The Fed even acknowledged its victory in explaining its 0.50% rate reduction in September by citing the inflation figures and expressing concern that unemployment numbers were starting to creep up over the summer, and they wanted to get ahead of what might be coming.

Part of investor concern stems from the slight uptick in inflation over the last quarter. However, this outcome was easily foreseen by looking at the low monthly inflation data scheduled to roll off from the fourth quarter of 2023. The same will happen next quarter in reverse; high monthly inflation data from the first quarter of 2024 will lower year-over-year inflation. None of this supports a higher inflation outlook.

Housing inflation is showing signs of slowing

Housing is the largest portion among the inputs for inflation calculations, but is usually 6-12 months behind anecdotal evidence of lowering rents. Rental rates reset as contracts slowly renew, so changes in rent today can take time to show up in broad inflation data. When PCE peaked in mid-2022, housing costs rose 4-6%. One year later, they were growing 7-8%. By the end of 2024, annual shelter increases slowed to 4-5%, reflecting the lowest month-over-month changes since the pandemic. Housing cost growth is finally decelerating. Like turning a cruise ship in the ocean, it won’t likely pick up speed again soon, keeping a lid on inflation growth for the immediate future.

Uncertainty over fiscal policy

Tariff threats from the new administration are driving a material portion of the uncertainty. In fact, the Fed bears some responsibility for the problem. Following the November meeting, Powell responded to a question about the effect of potential fiscal policies on the economy: “We don’t guess, we don’t speculate, and we don’t assume.” At the December meeting one month later, in response to why Fed forecasts lowered rate cut forecasts in 2025 from four to two and increased inflation projections, Powell responded with, “some (members) did identify policy uncertainty as one of the reasons for their writing down more uncertainty around inflation”. While incorporating casually proposed and unpassed fiscal policy into economic forecasts may be “common sense thinking,” as argued by Powell, it also represents a deviation from its self-proclaimed data-driven focus in setting monetary policy.

While some tariffs will increase, to be sure, the topic is primarily a negotiating tactic. Some objectives will be economic (China: make trade more balanced), though others will be demographic (Mexico/Canada: police your borders better) and defensive-minded (Europe: spend more on military assets). If inflation starts increasing, excessive tariffs aren’t likely to be the sole source, though they won’t help.

Inheriting a moderate economy with softening inflation allows the new administration to pursue its policy goals more flexibly, pressing for lower rates, better trade conditions, and greater growth. We think the trajectory of both short- and long-term interest rates is more likely to be downward than upward.

Disclosure: This is for informational purposes only, and any reference to a specific company or type of security does not constitute a recommendation to buy or sell that company or security. The reader should not assume that an investment in the security identified or described was or will be profitable. For a complete list of disclosures, please click https://mitchcap.com/