Worldwide equity markets advanced 6.2% last quarter, bringing this year’s total return to 13.9%. Solid earnings reports, strength in the employment market, stabilizing banking fundamentals, and investors’ focus on artificial intelligence all contributed to the results.

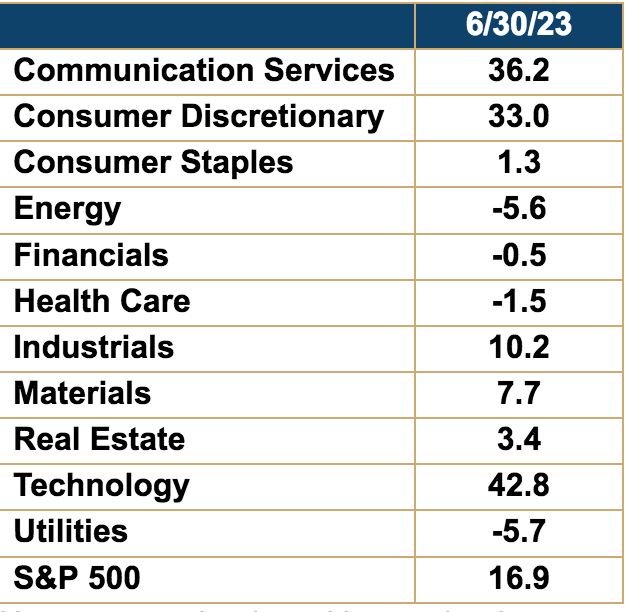

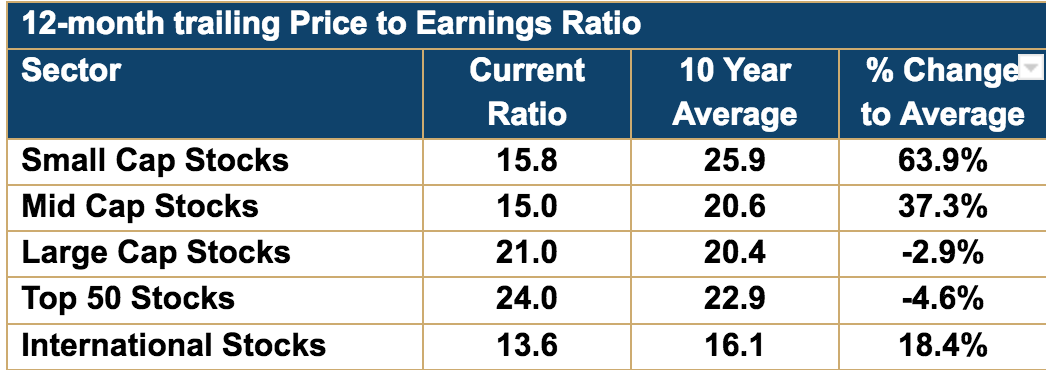

However, market breadth remained narrow for most of the quarter with only three of the eleven sectors having outperformed the broader index this year, while four posted negative returns. Larger capitalization stocks also outperformed their small and mid-capitalization counterparts. We expect the market breadth to expand over the next year as valuations are more attractive in small and mid-cap companies, and their business prospects remain underappreciated.

Valuations alone are not enough to spark investor interest, but the combination of attractive valuations and good earnings prospects will expand market breadth. The recent artificial intelligence (AI) enthusiasm has propelled large-cap technology-oriented stocks to above-average valuations while leaving most of the market behind. International stocks also look compelling as the foreign markets manage inflationary pressures and economic prospects improve.

Amara’s Law is the idea that we tend to overestimate the impact of technological changes in the short run and underestimate the impact of technological changes in the long run. This idea applies today as AI company valuations have expanded to historically high multiples.

We anticipate taking advantage of the valuation disparity by reducing near-term overvalued positions and adding high-quality small and mid-cap domestic and foreign stocks.

We monitor the consumer’s fitness by watching employment, spending, and credit card data. Overall, the employment market looks healthy as health care, construction, and retail trade gains offset job losses in technology and financial services.

Some consumers have reentered the workforce as inflation has impacted household budgets, and others, such as healthcare workers, have returned after taking some time off. Spending and credit card data remain robust as the appetite for travel and experiences has replaced spending on household items.

As we dig deeper into the credit card data, we see inflation negatively impacting lower-income households while higher-income households manage the situation better. Delinquency and charge-off rates for lower-income households have returned to normal levels last seen in 2019, while those for higher-income households are still below 2019 level, though modestly rising.

These changes translate to a shift at retailers as consumers trade down from brand name items to lower-cost private label items, and the stores are experiencing increasing levels of shrinkage (theft). These challenges have impacted stock prices, providing an opportunity to invest in high-quality companies that can manage and fix these issues over the next few years.

Financial companies have rebounded off their lows during the bank crisis in March, and the largest financial institutions recently passed the Federal Reserve’s stress test to confirm their stability. Valuations in this sector are also attractive and have built in the anticipated FDIC insurance increase, higher capital standards, more regulation, and increased funding costs. We are analyzing several company balance sheets and growth prospects to find a new investment opportunity.

Every economic, geopolitical, and financial scenario provides opportunities for investors to make solid long-term investment decisions. We’ve identified a few areas to research and look forward to updating you on these as they arise.

Fixed Income Markets

The Federal Reserve currently targets an overnight federal funds rate in the U.S. at 5.0%-5.25%. The lowest measure of core inflation is PCE core inflation at 4.6% year over year.

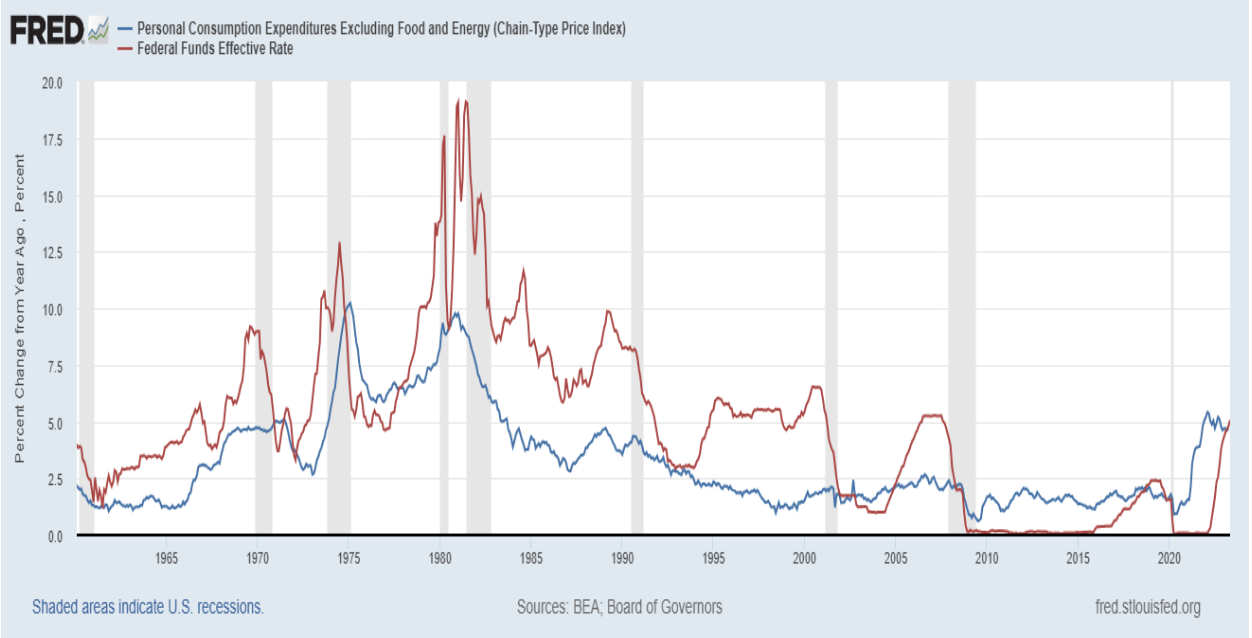

The graph below shows the historical relationship between core inflation and the overnight rate. Economic history is clear that elevated core inflation will persist until the overnight rate is at least two percent above the core rate and kept there for an extended period.

Arthur Burns, former Federal Reserve Chairman from February 1970-December 1977, said in 1979: “In principle, no matter how high the nominal interest rate may be, as long as it stays below or only slightly above the inflation rate, it very likely will have perverse effects on the economy; that is, it will run up costs of doing business but do little or nothing to restrain overall spending.”

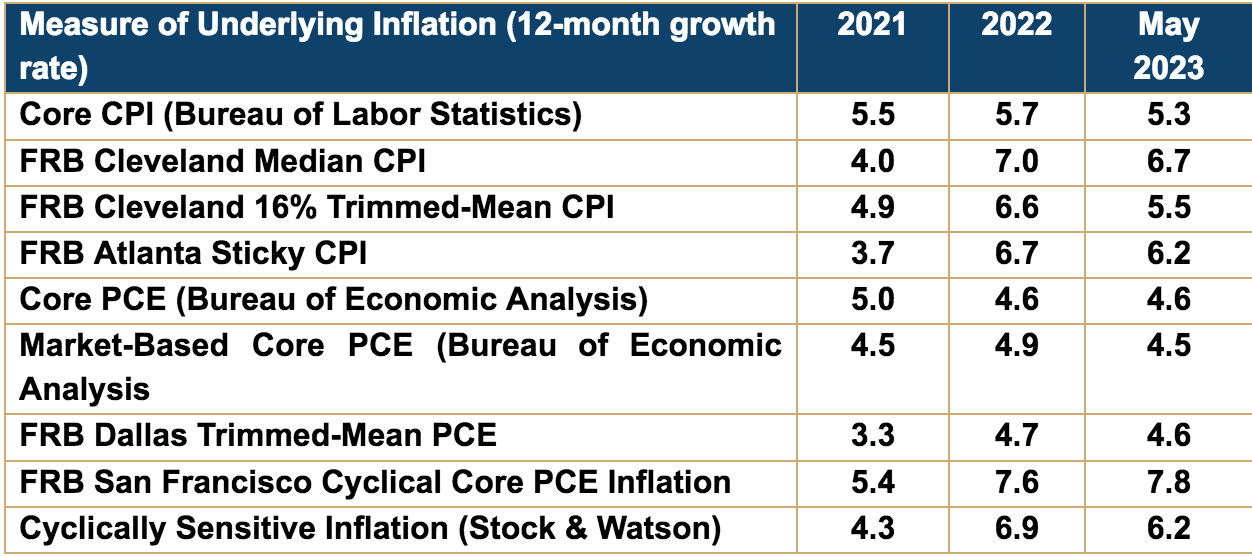

Projecting the likely path of inflation over the near term is a primary mission of the Federal Reserve. In pursuit of this objective, they focus on core inflation, stripping out the volatile components of food and energy. One challenge is that economists calculate inflation in many different ways. The table on the next page lists nine measures of inflation for the twelve months ending May 31, 2023.

For the twelve months ending May 2023, the lowest measure of underlying inflation is Market-Based Core PCE, calculated by the Bureau of Economic Analysis at 4.5%. The Cyclical Core PCE inflation at 7.8%, calculated by the Federal Reserve Bank of San Francisco, is the highest. No matter the measure, underlying inflation remains well above the Fed’s two percent target. The numbers in this table do not support the FOMC’s current projection for Core PCE inflation to decline to 3.9% by the end of 2023.

Central banks in Norway and the U.K. recently announced half-point interest rate increases to address persistent inflation. After brief pauses, Canada and Australia recently resumed rate increases, citing higher services-sector inflation and tight labor markets. The President of the European Central Bank (ECB), Christine Lagarde, at an annual symposium in Portugal recently, signaled the central bank would likely raise interest rates in July to tame high inflation. She noted that they expect Eurozone wages to grow in aggregate by 14% through the end of 2025.

At the same event, Fed Chairman Jerome Powell said, “The labor market is really pulling the economy. Over the past few months, you see stronger than expected growth, tighter than expected labor markets, and higher than expected inflation.” Global central banks are reversing their official views to acknowledge persistent inflation fueled by a heightened wage inflation cycle.

Thus, as history tells us, if core inflation remains stuck in the 4.5%-5.0% range, the Fed will have no choice but to raise the overnight rate to 6.5%-7% to get inflation back to its target. This environment will cause interest rates to remain elevated until monetary policy makes material progress on reducing inflation.