Equity Markets

Global equity markets advanced 8.2%, led by a 10.6% return in the US and a 4.7% advance in the international markets. Economic growth remains solid, and central bankers worldwide are reviewing monetary policy actions for the next steps in their respective inflation fights. We expect worldwide equity markets to continue advancing throughout 2024 with an occasional pullback.

Major investment themes, including artificial intelligence (AI), data warehouse expansion, and weight loss pharmaceuticals remain intact. We anticipate broadening of the market so that more sectors, industries, and individual companies can participate.

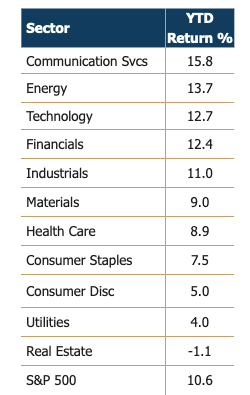

Recall that three sectors led returns last year by a large margin over the others: information technology, communication services, and consumer discretionary. But 2024 is about more than the themes above, with more industries participating in the advance, including the energy, financial, and industrial sectors.

Energy rose 13.7% last quarter as oil prices rebounded. Energy demand has and will increase as economic growth improves around the world, and the US Strategic Petroleum Reserve, at historic lows, works to rebuild its stockpile. Meanwhile, supply constraints allow producers to maintain higher selling prices, with the three largest having little to add. Saudi Arabia announced plans in January to halt their planned increase of one million barrels per day. Ukrainian drones and sanctions hamper Russian production and delivery, and US producers remain focused on prioritizing the return of capital to shareholders over drilling new wells. These factors will help keep oil prices higher.

Financials increased 12.4%, continuing to rebound from the significant decline during the banking crisis in 2023. The bank industry index advanced 15.3% last quarter, bringing the one-year gain to 45.8%. While still concerning, headwinds over office property loans have been manageable so far. Insurance companies participated with a 16.7% gain last quarter. Insurers have raised premiums as costs to replace or rebuild properties have risen. Additionally, their investment portfolios will benefit as they reinvest at higher interest rates.

Industrials increased 11.0% as investors anticipated the beginning of Federal Reserve rate cuts and a continued economic expansion. Companies exposed to data warehouse construction, infrastructure building, and transportation fared the best.

The market is broadening in other ways. Mid-capitalization securities started to participate as their valuation discount to larger companies became too vast to ignore despite solid revenue and earnings growth. Small-capitalization stocks have yet to close the gap, but the same supportive revenue and earnings growth applies here, too. We expect that gap to narrow as investors’ positive outlooks move down the capitalization chain. We are looking for and adding mid and small-cap companies to take advantage of these opportunities.

The US election is approaching quickly. We anticipate escalating rhetoric leading to and beyond November, but we expect our government to remain divided, usually the best outcome for investors. Spending, debt issuance, Medicare, and Social Security are major issues Congress needs to address, but legislative agreement and action will be elusive.

We have positioned our equity strategies well, but we remain focused on monitoring the current investment themes, looking for new trends, and adjusting individual company positions as valuations extend or business foundations change. We look forward to discussing the stock market, economy, US elections, and shifting monetary policy in our upcoming meetings

Fixed Income Markets

We are nine months from the last overnight interest rate increase and all eyes are on the anticipated pivot to lower rates. Yet inflation declines appear to have stalled and year-over-year measures remain uncomfortably elevated. Investors are starting to notice.

At year-end, bond prices reflected investor expectations for the Fed to lower rates 6-7 times by the end of 2024. Forecasts from the Fed itself, through its December Summary of Economic Projections (SEP), suggested three, a material disconnect. Following three months of strong economic growth, continued low unemployment, and higher-than-expected inflation data, sentiment contracted to two reductions, concluding that the Fed will be lowering less aggressively. Indeed, that shift drove the 10-year US Treasury note yield from a low in late December of 3.88% to 4.42% as we go to print.

Inflation remains a problem. In our last letter, we discussed the Fed’s difficulty easing inflation into its 2% target. The data underlying inflation calculations suggested it would be very hard, and the hurdles have only grown. Consider energy, whose declining prices deserve the primary credit for inflation’s decline over the eighteen-month period ending December, 2023. With oil up 21% and gasoline up 32% this year, energy prices are boosting inflation back upward. With demand finding a bottom as Europe and China return to growth, ongoing conflict in the Middle East, and major producers moderating output for various reasons, stable or higher energy prices are our base case going forward.

Second, many economists expected that a slowing of housing costs would be the missing ingredient to push inflation solidly towards the Fed’s 2% target. That hasn’t happened, and likely won’t. Even in our new, higher rate environment, which should be considered normal viewed in light of historical average mortgage rates, demand remains strong. At the same time, supply will continue to fall far short of what is needed. Most surveys estimate the housing shortfall in the millions of homes. The idea of declining housing costs in such an environment seems fanciful. We expect shelter costs, roughly 35% of CPI, to continue growing 4 – 6% annually.

Third, fiscal policy presented a material headwind against monetary policy. As the Fed tightened access to funding, Congress kept pandemic-level spending despite COVID being well centered in the rear-view mirror. For perspective, the 2019 budget deficit for the US Treasury was merely $0.984 trillion. The 2020 blowout produced a record-setting deficit of $3.1 trillion, and 2021 was only marginally less at $2.7 trillion. 2022 and 2023 budget deficits were better, but only by comparison at $1.4 trillion and $1.7 trillion, respectively, and 2024 is continuing the trend. Such continuing levels of budget-busting fiscal spending push against the inflation-fighting efforts of Fed policy, rendering the rate increases to date even less effective than they would be otherwise. No evidence suggests Congress will adjust its spending habits unless forced to do so.

In fighting inflation, the Fed knew the last steps towards 2% would be the hardest, and they are experiencing that now. The last three months of data interrupted the downward progression. Three months could be a head fake, the start of another leg upward, or something far stickier and reflective of a longer-term residence in the 4% range.