Equity Markets

US equity prices fell just over 3% during the quarter as the sugar rush of cheaper valuations, a Fed nearing the end of its hiking cycle, and the excitement of artificial intelligence (AI) began to wear off. Energy was the lone shining star of the quarter, with the sector moving up 12% following substantial production cuts from Saudi Arabia and Russia. The remaining sectors were flat or down on the quarter in what felt like a brief repeat of 2022. With interest rates soaring during the quarter, rate-sensitive utility and real estate companies fell 9%.

We spoke last quarter about the need for more market breadth. The indices felt like they were being pulled higher by just the “Magnificent Seven” Mega-Cap technology names. The majority of them took a breather this quarter as Google, Meta, and NVIDIA were each modestly higher, while Amazon, Tesla, Microsoft, and Apple ended lower. We noted in our last letter that multiples of AI-related names may have gotten ahead of themselves. Meanwhile, our expectation for wider participation from the rest of the market has yet to fully pan out. Small and mid-cap (SMID) sized companies have yet to gain a foothold, declining low single digits during the quarter.

Where to for the balance of 2023? Despite a -3% quarterly loss from the S&P 500, the index remains up a solid 13% on the year. With consensus forward earnings on the S&P 500 of $238, the primary index stands at 18x forward earnings. When compared to valuations of the last five years, this feels reasonable. However, major differences between then and now include an inverted yield curve, a 10-year Treasury that closed the quarter at 4.57%, oil above $90, and a consumer squeezed by higher interest rates and inflation.

Speaking of a squeezed consumer, the San Francisco Federal Reserve recently released a blog post entitled “Excess No More? Dwindling Pandemic Savings” in which they present the case that as of March 2023, the US consumer had just $500B of the $2.1T in total savings accumulated through the relief programs. If true, their math shows that excess is now likely exhausted and the US consumer may be under more pressure than we currently appreciate. Especially for lower-income households where credit card data shows much higher card balances and credit deterioration.

While the interest rate picture has clouded our outlook, there are also reasons for optimism. Core PCE (the Fed’s preferred measure of inflation) has fallen from 4.9% at the beginning of the year to 3.9% through August. It’s important to remember that core PCE excludes volatile food and energy prices, which have increased again and could change quickly. If inflation continues to subside, this should reduce pressure to the short end of the interest rate curve for the time being, ultimately helping to underpin equity valuations.

Additionally, the eerily quiet Initial Public Offering (IPO) market, which has been virtually closed since early 2022, has begun to show strong signs of revival. September welcomed the two largest IPOs in nearly two years, with ARM and Instacart (Maplebear). Markets accepted both names warmly, with first-day increases of +25% and +12%, respectively. These precedents should help thaw the IPO market for other private equity and venture capital-backed companies with public liquidity aspirations, helping remove some interest rate sand from the market gears.

With a solid start to 2023 and disinflation taking hold, it is tempting to feel that the Federal Reserve has engineered the previously improbable soft landing. No doubt this is what equity markets are currently pricing, leading two of Wall Street’s biggest bears for 2023, Bank of America’s Savita Subramanian and Morgan Stanley’s Mike Wilson, to walk back their calls for significant drawdowns in the stock market this year. Wall Street consensus is for 11% growth in earnings for 2024 due to continued softening in inflation, a robust labor environment, and Fed rate cuts. To the contrary, this raises our suspicions. History shows we have never successfully navigated an inverted yield curve in the modern financial era without a significant recession. Is this time different? It’s tough to say, so we remain fully invested yet cautious.

Valuations in SMID-Cap companies remain reasonable compared to some of the larger-cap technology companies that carried the banner for the year’s first half. Below the surface, there are great opportunities in many businesses that don’t regularly make the headlines of the Wall Street Journal.

We remain constructive on the energy (as we have been for two years now), technology, and communications sectors. We have started reviewing opportunities for companies that may prosper during flat interest rate periods, usually found in sectors like utilities, financials, and real estate, all of which have underperformed in 2023. We also see an opportunity to buy select financial names with robust balance sheets and great growth profiles at considerable discounts to historical multiples.

We have been moderately underweighted technology companies in 2023, but we expect that to increase over the next quarter. Despite technology being one of the strongest performing sectors, the underweight hasn’t sacrificed performance due to strong stock selection by the equity team. 2023 has been a stockpickers market and we believe that will remain the case into next year as well.

Fixed Income Markets

The Federal Reserve raised overnight rates by 0.25% in its July meeting and made no changes at its September meeting, leaving the overnight rate at 5.5%. However, the real action occurred with the 10-year U.S. Treasury yield which moved from 3.81% to 4.57% as investors realized a steady reversal of inflation to 2% was premature. We have rarely been happier to hold short-dated portfolios than this quarter, providing positive returns while bond benchmarks were negative.

Higher terminal rate, and for longer – the terminal rate is the point where the Fed stops increasing the overnight rate. Many investors hoped the July increase was the last, yet as long as unemployment remains near historical lows, and GDP growth continues to exceed forecasts, it becomes clearer that the inflation fight isn’t done. Investors fear the Fed may need to take a harder line (re: more rate increases) to arrest inflation and force it back to 2% the hard way, compared to the easy downward trend we have experienced since last summer. It’s not at all clear we are at, or near, the terminal rate and investors are nervous.

Higher deficits – it’s no secret the US Treasury is running record-breaking deficits, without a pandemic or war on which to place blame, and interested parties are taking notice. On August 1 2023, Fitch downgraded the credit rating for the US to ‘AA+’ from ‘AAA’. S&P did the same in 2011 in the middle of another debt ceiling fight. And while the Federal Reserve is neither adding to its bond portfolio, nor replacing maturities with new purchases, the US Treasury must fund the spending blowout with new buyers and interest costs on current debt are growing rapidly.

We have followed several other issues that haven’t concerned investors yet, but may at some point: the growing operating losses on the Federal Reserve balance sheet which now exceed $110 billion, unrealized losses on the Fed’s bond portfolio exceeding $1.5 trillion, and Fed responsibility for investment losses on bank bond portfolios that led to liquidity problems in March.

The Federal Reserve repeatedly states their intent to raise rates enough to slow inflation and keep rates high until inflation was clearly moving towards the 2% target. At the same time, Fed forecasts were calling for rate decreases next year. In our view, this is saying one thing and forecasting another. Then the latest forecast released in September suggested fewer rate cuts in 2024 than previously thought (two instead of four) contributing to the higher rates above. We’ve asked this before, but maybe Fed forecasts haven’t earned the attention they enjoy.

Four times each year, the Federal Reserve updates its Summary of Economic Projections (SEP) forecasting the unemployment rate, change in GDP, headline inflation, and core inflation. The central tendency forecast drops the three highest and the three lowest to identify a range. Over the last five years, 67 forecasts have been distributed, and the results aren’t encouraging. Final GDP fell within the forecast range nine times – 58 times final GDP fell outside the forecast central tendency range. They did worse with final inflation results, which fell into their forecast range only five times, recording 62 inaccurate inflation forecasts. They whiffed entirely in 2018, 2021 and 2022 when most inflation forecasts ended up too low. Keep this in mind when the Fed talks confidently of inflation heading back to its 2% target while projecting 3.3% inflation in 2023 and 2.5% in 2024. Such a poor record demands investors heavily discount Fed inflation forecasts, review the available data independently, and draw their own conclusions.

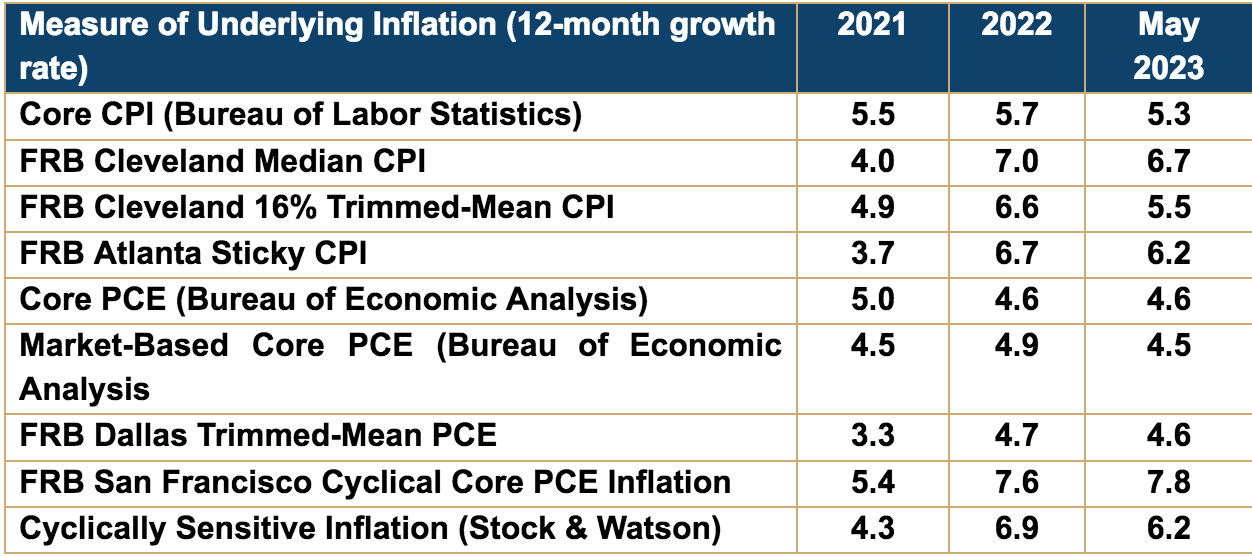

The table reflects several inflation measures which, taken together, show price levels to be sticky despite numerous rates increases. While down from highs last summer, they are still more than twice the target level. And a quick look around shows headwinds in inflation inputs that matter most. In the first case, consider rising energy prices. With two of the three biggest oil producers (Saudi Arabia and Russia) delivering less inventory to world markets, and the third (the U.S.) not picking up the slack, it becomes an open question how long elevated energy prices will be around.

Second, the labor market remains tight with near-record low unemployment. Data from the Atlanta Fed reports annual wage growth exceeding 5%, but given the cumulative price increases over the past three years, workers are still feeling left behind, keeping concerns about a wage-inflation spiral alive and well. The upshot? Getting inflation back to 2% is going to be difficult and bond investors are right to be concerned.

Disclosure: This is for informational purposes only, and any reference to a specific company or type of security does not constitute a recommendation to buy or sell that company or security. The reader should not assume that an investment in the security identified or described was or will be profitable. For a complete list of disclosures, please click https://mitchcap.com/