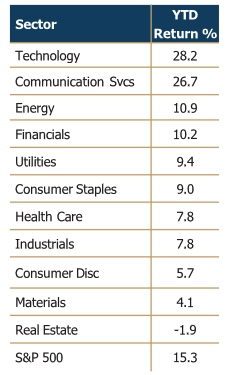

Equity Markets

Global equity markets continued to advance this quarter, with the US market up 4.3% versus an international market return of 1.2%. The second quarter was more muted than the first but included a solid round of earnings reports from many companies. Interest rates continued to rise as inflation remained stubbornly within the 3.0 – 3.5% range, higher than the Federal Reserve’s 2% target. The global economy’s ability to sustain these high interest rates is a positive sign for continued economic progress. Coupling this with the low unemployment rate and a slowly recovering labor participation rate paints an even brighter picture.

Technology companies are increasing broad market returns due to tangible and significant spending on new and expanding artificial intelligence (AI) applications. Enterprises large and small are investing billions of dollars to automate operations and create efficiencies.

These AI possibilities have translated into real dollars today for specific industries.

- Utilities such as electricity producers have seen increased demand as data centers expand nationwide.

- Semiconductor producers are experiencing a substantial price premium from customers willing to pay for the fastest and most efficient chips.

AI is in its infrastructure-building phase, which brings with it the winners and losers in laying the physical groundwork. AI has a long growth runway as more and more tasks are automated.

Meanwhile consumers continue to spend and are increasingly divided into two groups. The first group has plenty of savings via earnings increases and the stock market rally during the last four years.

The second group has experienced fewer wage gains plus inflation of the last four years without corresponding market gains.

- The first group is spending a lot on services like travel, entertainment, and dining out.

- The second group is searching for value as much as possible to better manage food and clothing inflation. Discount stores are the prime beneficiaries, as apparel and food comprise a sizable portion of this consumer’s budget.

Energy companies had a volatile quarter. Lower expected global demand, higher US production capacity, and expiring OPEC cuts were the main culprits, pushing oil down 15% before OPEC extended and added new production cuts to its 2025 plan. US-based energy companies will likely capture this price benefit and return it to shareholders in the form of dividends and share repurchases.

Large banks and insurers led financial companies as they took advantage of higher interest rates to increase the value of their investment portfolios. Credit service companies have seen a growing number of consumers struggle to make payment schedules, pushing delinquency rates up.

Central banks have been reacting to inflation data differently:

- The US Fed, Bank of England, and Reserve Bank of Australia have left rates steady for almost a year.

- The European Central Bank (ECB) ended its 2-year period of increasing rates by lowering on June 12.

- The Swiss National Bank has been reducing rates since March.

Although there is considerable desire among equity market investors for a lowering of interest rates, the timing of such decisions is uncertain. Nevertheless, the ability of central banks to use the monetary policy lever should help mitigate any economic issues that may arise in the future.

Many businesses have been delaying projects, such as expansion or new initiatives, as they wait for interest rates to move down. Consumers have the same mindset toward larger purchases that must be financed. If and when rates fall, a significant economic catch-up may materialize. In the meantime, your portfolios are positioned to benefit if rates are left unchanged.

Fixed Income Markets

Interest rates were flat during the 2nd quarter but not without movement. Investors continued to adjust forecasts of when the Federal Reserve would start to move interest rates down and by how much. The 10- year U.S. Treasury Note peaked at 4.7% on fears that the Fed may not be restrictive enough, meaning they would have to reverse course and raise interest rates. The Fed’s current forecast is for one rate lowering in 2024, reflecting its waning confidence that inflation is descending as quickly as expected.

Our assessment is that the Fed will not be able to lower interest rates in 2024 because, by year’s end, it will become evident that inflation is stuck at the 3%-4% level. Persistent inflation is the primary economic consequence of fiscal and monetary policy responses to the COVID-19 pandemic. As a reminder, the collective $5.9 trillion fiscal policy response from Congress included the CARES Act ($2.2 trillion, of which

$0.8 trillion was for the Paycheck Protection Program), Consolidation Appropriations Act ($0.9 trillion), American Rescue Plan ($1.9 trillion) and the most recent Inflation Reduction Act ($0.9 trillion). Monetary policy responses from the Federal Reserve included cutting interest rates to 0%, large-scale purchases of Treasury and mortgage-backed securities (the Fed purchased over half of the new debt issued to fund these fiscal policies), and emergency lending facilities.

The Federal Reserve is keenly focused on restoring inflation to its 2% target following the surge in 2021, which peaked at 9.1% one year later. Realizing it had incorrectly forecasted inflation to be ‘transitory,’ it took steps to reduce its accommodation in 2022 by reducing the size of its balance sheet and increasing the overnight rate from 0% to 5.3% before stopping in July 2023.

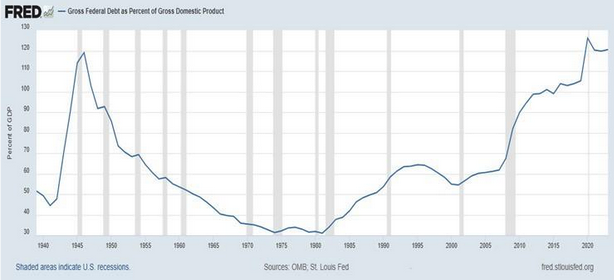

Fiscal policy remains in emergency mode. 2024 deficits are forecast to be $2 trillion, exceeding the $1.7 trillion deficit in 2023. Considering debt as a percentage of GDP, the graph below shows that ratio now exceeds the level at the close of World War II and will need to be addressed similarly to the period between 1946 and 1965. In the meantime, the need for a more restrictive monetary policy (keeping interest rates higher for longer) to compensate for the spendthrift fiscal policy is urgent.

Disclosure: This is for informational purposes only, and any reference to a specific company or type of security does not constitute a recommendation to buy or sell that company or security. The reader should not assume that an investment in the security identified or described was or will be profitable. For a complete list of disclosures, please click https://mitchcap.com/