Equity Markets

Rebound

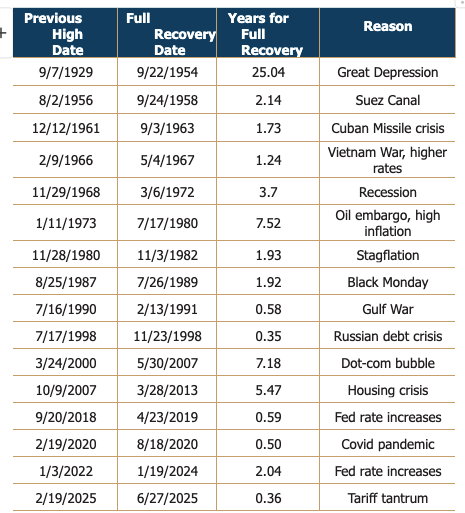

The S&P 500 was officially introduced in 1957, but a legacy version of the index was released 30 years prior, in 1927. In the nearly 100-year history of this S&P Index, 16 periods experienced a 15% or more drop from the previous high.

The first instance was also the worst: the Great Depression. If someone had invested at the peak on September 6, 1929, it took them over 25 years to break even (not inflation-adjusted). Over time, recovery periods have generally shortened, with two notable exceptions: the dot-com bubble of 2000 and the housing crisis of 2008.

Several insights can be drawn from this history, but perhaps the most important is this: recoveries can be extremely swift. One of the biggest mistakes an investor can make is selling at the bottom and not participating in the rebound.

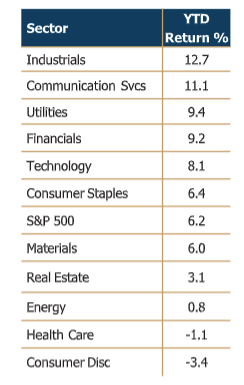

This quarter was a rebound and demonstrated typical sector alignment, led by the more growth-oriented names that declined the most in the first quarter. Prominent AI-related companies led the technology and communications sectors (see next page), which is encouraging as the data center trend regained its footing.

According to our calculations, data center exposure (across multiple sectors) has reached about 40% of the S&P 500, making it the dominant investment theme. We have decided to overweight this segment by increasing allocations to the more stable components of data center growth: construction, electrical power supply, security, and connection hardware. All will be necessary, regardless of who is building the data center or who wins the AI race.

What’s Next?

This year, the central theme has been tariffs pursued by the current Presidential administration. With rhetoric and ramifications running high, these policy changes were of great importance to the investor community—especially as drastic changes were made on a near-daily basis. For now, many of the tariffs are paused for negotiations, but talks can be fickle, bringing in one thing the market perhaps dislikes the most: uncertainty.

Where will tariffs go?

It is difficult to predict, as outcomes appear to hinge on decisions made by a single individual—the President. However, no elected official wants to inflict economic pain on their constituents, and there would likely be fierce political blowback if tariffs begin to significantly impact American consumers. Encouragingly, the administration’s decision to pause the tariffs came after bond yields jumped following “Liberation Day.”

How will the tax and spending bill affect individuals and markets?

On July 4, the tax cut and spending bill, H.R. 1, was passed into law. Sustaining lower tax rates and eliminating taxes on tips and overtime should promote economic growth. However, the cost will be felt in the healthcare sector, where Medicaid enrollment is expected to decline by about 12 million people.

Additionally, $3.4 trillion will be added to the U.S. public debt, which could create more volatility in the fixed income markets and raise the specter of inflation, potentially resulting in higher interest rates.

What’s next?

The S&P 500 is up 6.2% through the first two quarters of 2025. Considering the historical average one-year return for the index is about 8%, we are currently on track for a strong year, despite both 2023 and 2024 having already returned over 25% each amid notable market turbulence.

The first-quarter earnings season was generally positive, with many companies showing steady consumer spending and continued investment. Although hiring has slowed, job layoffs and the unemployment rate have not yet increased.

For now, the U.S. economy appears to have weathered the storm and may benefit from a combination of lower tax rates, stable or relaxed interest rates (if inflation eases), and rising productivity driven by AI. We will continue monitoring the second-quarter earnings season to evaluate these key indicators.

Thank you for your continued trust. We look forward to speaking with you at our next meeting.

Fixed Income Markets

The Federal Reserve left the overnight rate unchanged in 2025, at 4.25% – 4.50%, primarily due to inflation and, most recently, the potential impact of tariffs on inflation, leaving the FOMC in a wait-and-see mode. We think they will be in that posture for the next 6-12 months.

In the flood of tariff announcements in April, levies applied to nearly every trading partner were increased, sometimes dramatically, as in the case of 145% duties on imports from China. Most tariffs beyond a 10% baseline were quickly suspended for 90 days on countries that hadn’t retaliated. July 9 is the new deadline, but it is anyone’s guess whether they will be suspended again. Beyond the public twists and turns of the tariff story, it seems probable that some level of additional tariffs will become permanent. It is also likely that most importers will pass along higher costs to their customers.

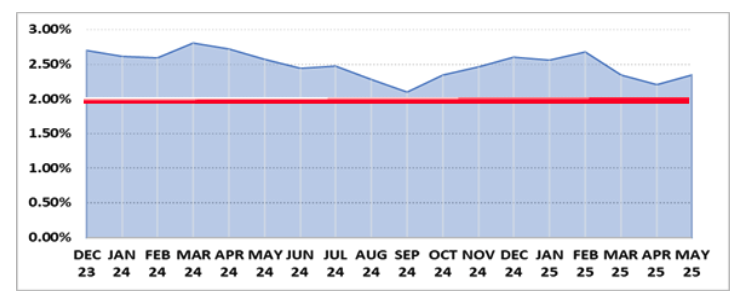

The Federal Reserve has officially targeted 2% inflation since 2012, an arbitrary objective and much too high. 2% inflation per year will strip 22% of an asset’s value over a decade. Why not target 1%, or even 0%? Last September, during a heated election season, the inflation rate touched 2.1% and the Fed reacted by lowering the overnight rate by 0.50%. Jerome Powell, Fed Chairman, without formally declaring victory, suggested that in their collective view, inflation was clearly on the path to the Fed’s 2% target.

However, as depicted in the following graph, while PCE has gotten tantalizingly close to the target, it has remained stubbornly above it, currently at 2.34%. To complicate matters, the Federal Reserve’s own projection calls for a 2025 inflation rate of 3%.

While tariffs garner the press, inflation is more than a problem of higher-priced imported goods, as anyone who has recently paid property taxes can attest. Household utilities are up 9.4% annualized over the last six months. Over the same period, auto insurance is up 6.5%, health insurance is up 4.1%, and homeowners insurance is up 5.3%. Even if the effect of tariffs is negligible, inflation at 2.34% and sticky service costs indicate that we’re not yet finished with the pursuit of stable prices.

The Fed has no need and a weak defense for reducing interest rates further at this time. However, one additional factor may come into play: political pressure. The history of the Federal Reserve is littered by administrations clamoring for lower rates, some of which applied pressure more discreetly than others. It’s why FOMC voters often proclaim independence from political influence, as a public reminder of their pursuit of policy purity. All of which raises the question of whether the FOMC’s current voting unanimity will hold.

Now, under similar data and a new administration, two camps have emerged among FOMC members: one larger, progressive set that forecasts zero rate cuts in 2025, while a smaller, conservative set projects two cuts. The evolution of the two factions bears similarities to the composition of the Supreme Court – another non-partisan institution that operates through the lens of conservative and progressive political appointees and whose outcomes incorporate those worldviews when managing policy based on imperfect data and forecasts.

To highlight but one example, in speeches following the June 2025 meeting, Fed Governors Christopher Waller and Michelle Bowman, both nominated by President Trump during his last term and members of the smaller conservative group, raised the prospect of rate reductions as early as the next meeting in July. They had pushed against rate reductions last September under similar conditions and a different administration. It’s widely known that President Trump wants the Fed to lower rates, and fast – a gift progressive voters would prefer not to deliver. Stay tuned.

Disclosure: This is for informational purposes only, and any reference to a specific company or type of security does not constitute a recommendation to buy or sell that company or security. The reader should not assume that an investment in the security identified or described was or will be profitable. For a complete list of disclosures, please click https://mitchcap.com/