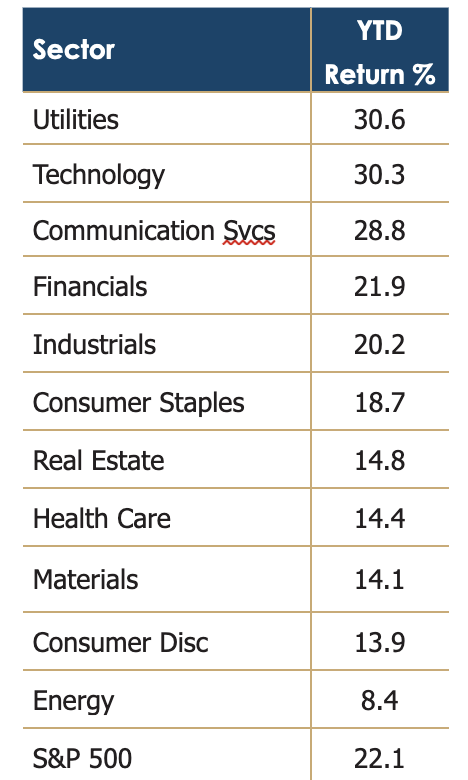

Equity Markets

Stock advances this quarter were led by international markets returning 8.1% while US markets rose 5.6%. Building on previous strong performance in the first half, global (including US) year-to-date equity returns now exceed 18.7%.

Economic growth remains solid, and the Federal Reserve took its first step in changing monetary policy from neutral to accommodating. That policy decision helped broaden participation, with more sectors and industries contributing in the advance. We expect worldwide equity markets to continue growing throughout the following year with an occasional pullback.

With the US election on the horizon, we anticipate a divided government. Historically, equity markets have responded positively to divided governments, reducing expectations that companies must adapt to dramatic policy changes, the most impactful of which incorporate the tax code. We will closely monitor the election results and make necessary portfolio adjustments.

Major investment themes, including artificial intelligence (AI) and data warehouse expansion, will remain strong, and we expect to see an improvement in economically cyclical and interest rate-sensitive industries. Investor confidence in cyclical sectors like industrials and materials is growing. They believe that easing worldwide monetary policy (the Fed is only the latest central bank to lower rates) will stimulate the global economy and increase demand for commodities, machinery, and household durable goods. The energy sector, in contrast, is facing challenges due to high production and supplies from OPEC and the US, reduced demand from China, and the resulting supply-demand imbalance.

Interest-sensitive sectors, like utilities and real estate, were the strongest performers last quarter. Lower interest rates reduce the financial burden of paying for business expansions and allow companies to refinance higher-cost debt. Utilities also enjoyed increased power demand as database warehouse expansion requires more electricity. Real estate valuations and transactions are increasing again, excluding office properties. The office market will need three to five years to recover from an ongoing oversupply, which may alleviate if companies successfully bring employees back to the office.

While there have been concerns about valuations and the profitability of the AI investment theme, it’s important to remember where AI stands in its evolution. AI has been around for years conceptually, but it has only recently become top-of-mind for business leaders seeking an edge and founders with a new idea – AI is still in its early stages. Like the Internet, and the personal computer, AI will open opportunities to help companies become more efficient and create new business lines, fostering profitable companies where it is leveraged well and liquidation where it isn’t.

Our investment strategies focus on companies that are generating revenue, cash flow, and earnings while maintaining an acceptable valuation and the process remains unchanged. During this early stage of AI, we have made successful investments in companies physically building the data centers needed to realize the potential of AI, companies that supply networking equipment to those data centers, companies that design and manufacture the sophisticated chips to run those data centers and companies providing the electricity to power those data centers.

Successful AI investments also include companies utilizing AI to help improve existing consumer products, digitize inefficient processes, and enhance cloud security. We are only at the beginning and we will continue to focus on new opportunities as they arise and AI-related applications expand.

The market is broadening in other ways. Mid-capitalization and small-capitalization securities have advanced as their valuation discount to larger companies became too vast to ignore especially when considered with improving revenue and earnings growth. These companies took a little longer to adjust to higher costs and interest rates. They have transformed themselves and are now poised to accelerate revenues with lower interest rates and an improving economic environment.

We have positioned our equity strategies well but remain focused on monitoring the current investment themes, identifying new trends, and adjusting individual holdings as valuations extend or business foundations change. We look forward to discussing the stock market, economy, US elections, and shifting monetary policy in our upcoming meetings.

Fixed Income Markets

As 2021 ended, criticism of the Federal Reserve mounted as the elevated inflation rate labeled ‘transitory’ by Jerome Powell, Chairman of the Federal Reserve, turned out to be ‘sticky’ instead. In March of 2022, Powell announced that the Fed would begin a program of raising the overnight interest rate to fight inflation and that it would not be painless – as they sought to slow the economy there would be job losses.

With two open jobs for every applicant, the Fed felt labor markets were misaligned with too much demand for the available labor pool. Over the next 18 months the Fed took the overnight interest rate up to 5.25% before pausing in September 2023, at which point the unemployment rate was 3.8%, still at an historically low level and only slightly higher than 3.6% in March 2022 when rate increases began. Meanwhile, inflation as measured by the Personal Consumption Expenditures Index (PCE) declined from 6.97% in March of 2022 to 3.42% in September 2023.

At this point, Powell made it clear that the Fed would think about lowering interest rates only when it was very confident inflation was on a sustainable path back to its 2% target. On September 18th, 2024 the FOMC decided to lower the overnight interest rate by 0.50%. In his press conference, Powell went to great lengths to state that the Fed was pleased with the progress made on inflation and in its judgement, inflation was on a sustainable path back to the 2% target. The Fed would switch its focus to the labor market.

The Fed is recalibrating monetary policy towards lower rates and a new rates program, but the timing is economically odd. Contrary to usual practice, it did so without the pressure of a recession, excessive job losses, or broken credit channels. In fact, economic conditions remain positive. Forecasts project the economy to grow at 3% through year-end, unemployment at 4.2% remains well below the 5% economists thought for years was the ideal level, and layoffs remain rare. Also, the cost of money aside, credit remains easy to obtain, corporate earnings growth is strong, and stock prices are near all-time highs.

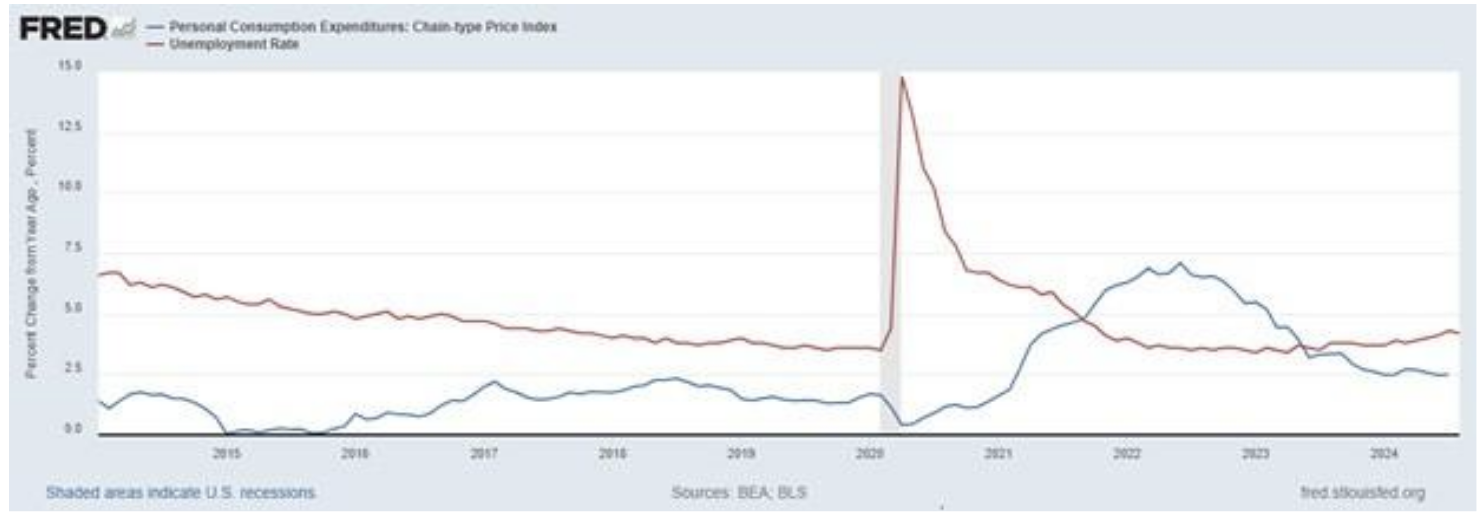

Inflation moving towards its 2% target (blue line below) provided the excuse to turn attention to the labor market. The Fed focused on unemployment levels creeping up from the 3.4% low posted in January 2023 (red line) and wants to preemptively deflect condemnation of lowering rates too little, too late, or not at all.

Fixed Income Markets

During the September press conference, in reference to the rate reduction program, Powell used the word ‘recalibration’ nine times. We would prefer he insert ‘cautious’ in front because while things are good now, we see risks on the horizon.

It is true that inflation has declined and will likely reach 2% with the September release. However, we think that inflation isn’t done with us, and will rise in the fourth quarter, for at least three reasons.

Services Inflation

Services such as housing, medical, and insurance costs make up 60% of the inflation index and are running

at a 4% annual rate. This part of the index has been slow to change trend.

Deficit spending

The US Treasury expects to spend $2 trillion more than the tax receipts it receives in 2024. Debt/GDP ratios (in the chart below) remain at historical highs, which is notable because we are not fighting a world war or pandemic. The Federal deficit has not emerged as an issue among the voting public and both Presidential candidates are content to leave it largely unaddressed.

A barrel of oil that cost $120 two years ago is down to $67 now. It is no coincidence that oil reached $120/ barrel around the same time that PCE inflation peaked at 7.0%. As energy prices subsequently declined, despite two regional wars, including one in the Middle East, so did inflation. While energy prices could go lower, it is unlikely. Goods inflation is negative largely due to the lower costs of transporting those goods. If energy costs, and by extension the cost of goods, even stand still, services inflation running at 4% will have a more significant impact on the overall price level.

Disclosure: This is for informational purposes only, and any reference to a specific company or type of security does not constitute a recommendation to buy or sell that company or security. The reader should not assume that an investment in the security identified or described was or will be profitable. For a complete list of disclosures, please click https://mitchcap.com/