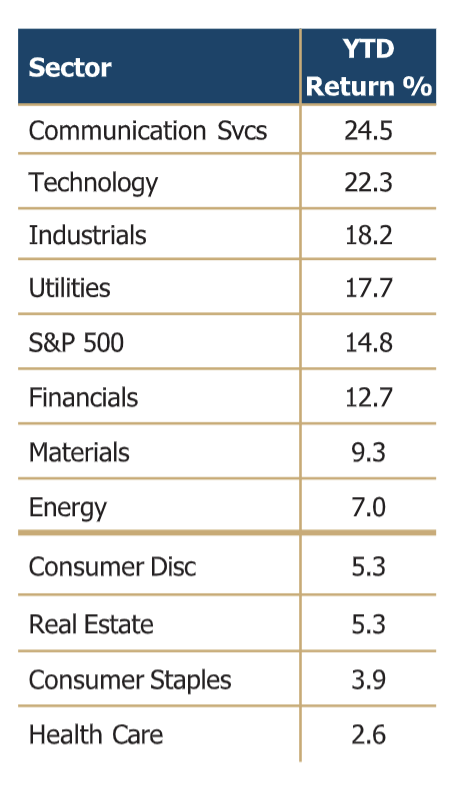

Equity Markets

Global equity markets continued to advance, with the US posting an 8.1% gain for the quarter and international markets advancing 6.9%. Solid economic growth, a resilient US consumer, Federal Reserve policy changes, and some clarity on tariffs and tax policy drove the gains. We expect equity markets to continue advancing as the Federal Reserve embarks on lowering interest rates, data center and Artificial Intelligence (AI) development continues, and the long-term potential of increased US manufacturing is realized.

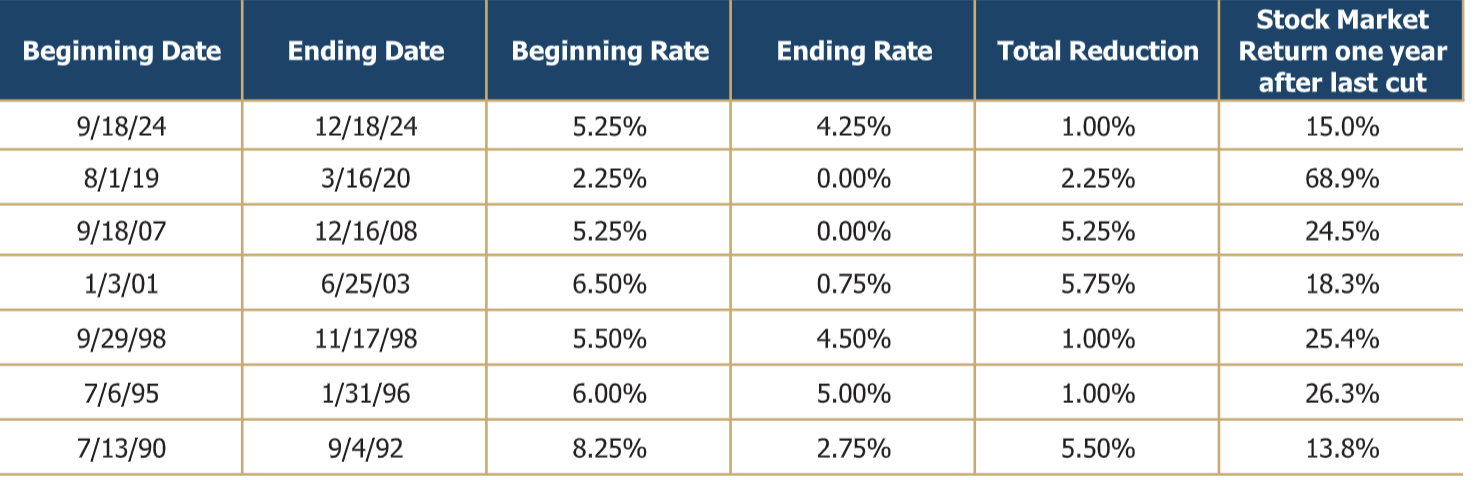

Stock market performance varies significantly throughout the interest rate cycle. As we examine past time frames when the Federal Reserve lowered interest rates, we see varied rates of return once it completed the cycle. The broader economic environment is a significant factor during an easing cycle, but a historical review is instructive.

The table below shows stock market returns one year after the rate cuts ceased. Each scenario was different; some experienced a recession, a mortgage/banking crisis, a currency crisis, or a technology internet bubble, while others were considered mid-cycle adjustments. With the Federal Reserve reengaging in the current lowering cycle, we don’t know when it will end, but history suggests a positive outcome for equity investors.

Current economic conditions are influenced by several factors, including tariffs, tax policy changes, immigration reforms, inflation over the past few years, and the data center and manufacturing buildout. The datacenter buildout is currently the most significant contributor to economic growth. We estimate

that this trend is impacting 40% of the US stock market capitalization. Companies involved in raw materials, building construction, energy/electricity production, computer systems, and semiconductors are all experiencing a positive impact on demand. How long this can last and whether it is like the 2000 internet bubble are questions on investors’ minds.

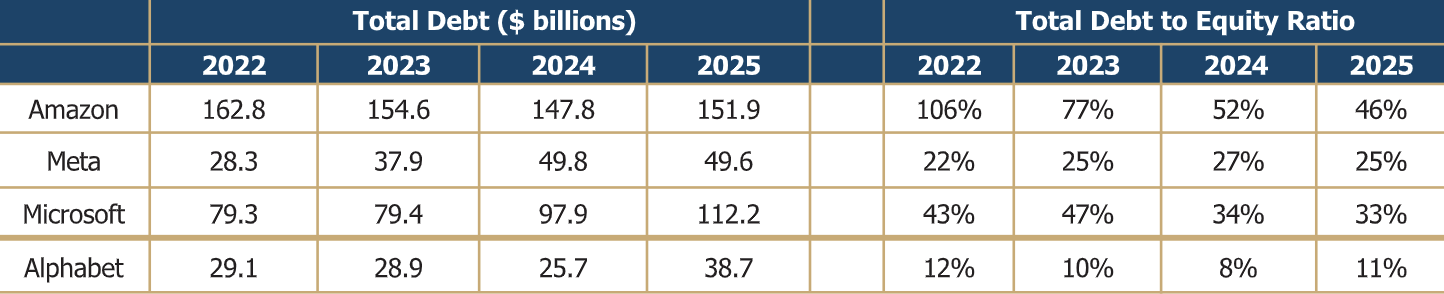

The large data center companies, including Microsoft, Amazon, Meta, and Alphabet, regularly appear to

make new $10 billion spending announcements. Unlike the internet bubble, these companies are generating revenues and cash from their businesses to fund the expansion. They are less reliant on debt issuance to finance their future. Examining the big four’s balance sheets reveals modest increases in debt

and stable total debt-to-equity ratios.

These companies have the financial capability to continue their expansion well into the future. Demand for data center services is a top priority in our equity research discussions. End demand will be necessary to keep these stocks and the other 40% on their growth path. Companies will continue to seek efficiencies, scalable new markets, and increased applications of AI. These drivers will continue to maintain a strong demand for data center services. New buildings, increased electricity demand, advanced computer systems, semiconductors, and scalable software will be necessary over the next decade and beyond. There will be periods of lackluster growth, primarily due to difficulties in securing construction projects that are zoned, approved, and physically built. Construction labor is in short supply and operating near full capacity.

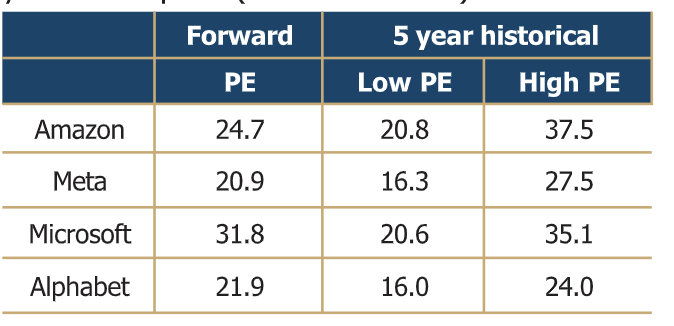

An investment theme like AI is not one to set and forget. Prospects evolve and change quickly, and we monitor valuations to determine if company stock prices are outpacing earnings potential. When they do, we will take the opportunity to reduce positions, diversify, and find other opportunities, steps we have already taken with several positions during the cycle. Currently, several AI-oriented companies have high valuations, but the data center companies are within historical ranges, suggesting that valuations are not yet at their peak (see table below).

We remain focused on monitoring current investment themes, looking for new trends, and adjusting our views on individual companies as valuations evolve or business fundamentals change. We look forward to discussing the stock market, the economy, and shifting monetary policy in our upcoming meetings.

Fixed Income Markets

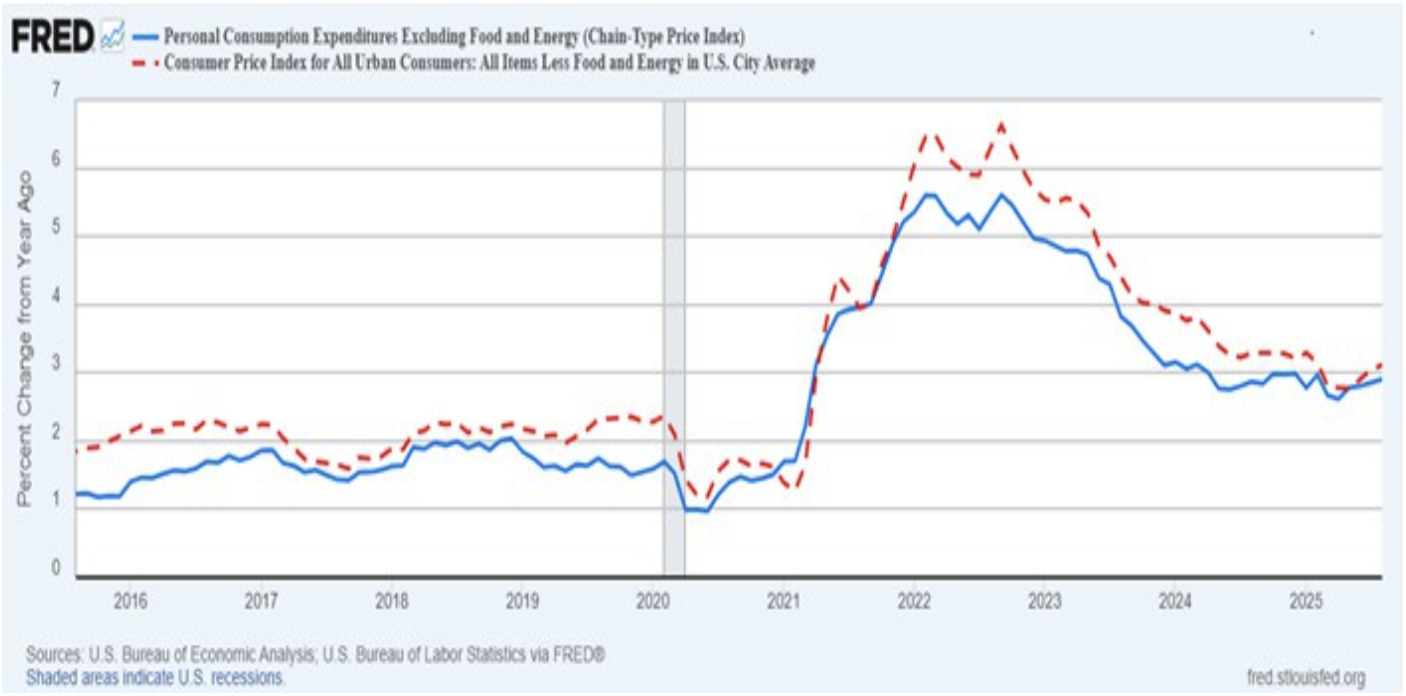

The Federal Reserve cut the overnight rate by .25% to a target range of 4.00% to 4.25% in September, even while inflation hovers around 3%. The FOMC statement cited a “somewhat softer labor market” while conceding inflation remains elevated. During his press conference, Federal Reserve Chairman Jerome Powell acknowledged the Fed’s commitment to restoring 2% inflation but stressed the need to weigh risks to both sides of its mandate, suggesting a more flexible approach to balancing inflation and employment.

Recall that in September 2024, the Federal Reserve made its first move of the current easing cycle, cutting the overnight rate by 0.50% (followed by another 0.50% by year-end), while core PCE and core CPI inflation measures were running at 2.87% and 3.29% respectively. Powell stated then that the Fed had “gained greater confidence that inflation was moving sustainably toward 2%.” He also noted that job gains had slowed and unemployment had edged up, signaling a cooling labor market.

Lowering rates again one year later, core PCE inflation, the Fed’s preferred measure, is currently at 2.91%, and core CPI is at 3.11%, essentially unchanged and still far from its 2% target. Although the greater concern may be that the Fed’s latest forecasts project core inflation will not return to 2% until the end of 2028, marking more than seven years of inflation running above target—a troubling admission for an institution tasked with maintaining price stability. Has the Fed abandoned its 2% inflation target?

Actions speak louder than words. And the collective actions of FOMC voters suggest the Fed is willing to let inflation run hotter for the foreseeable future. Neither the stock nor the bond markets are currently holding the Fed accountable for inflation above its target. The Fed will continue to lower the overnight rate to stimulate the economy until inflation reaches an uncomfortable level.

The Federal Reserve’s approach to monetary policy has evolved over several decades. From the years of Paul Volcker, Fed Chair from 1979 – 1987, who aggressively raised the overnight rate to fight double-digit inflation, followed by Alan Greenspan, Fed Chair 1987 – 2006, whose vagueness was almost an art form when speaking about monetary policy, to Ben Bernanke, Fed Chair from 2006- 2014, leading the charge on inflation rate targeting that was officially adopted in 2012. Note that the 2% target was neither mandated nor approved by Congress, but rather is an internal guideline intended to reflect the Federal Reserve’s view on how to maintain price stability.

Investors typically ask three questions when the Federal Reserve is contemplating adjusting interest rates. 1) When will they start? 2) How far will they go? 3) How fast? We have the first answer. They lowered the rate by 0.25% at the last meeting in September. The current Summary of Economic Projections dot plot shows a wide range of opinions on how far to take the overnight rate and how fast. We anticipate that by mid-2026, the overnight rate will be at 3%.

It is very easy to get lost in the minutiae of what different Fed officials are saying. Instead, we need to watch what they’re doing. The FOMC scheduled its next meeting for October 28-29. The next move could be a 0.25% or 0.50% reduction.

Disclosure: This is for informational purposes only, and any reference to a specific company or type of security does not constitute a recommendation to buy or sell that company or security. The reader should not assume that an investment in the security identified or described was or will be profitable. For a complete list of disclosures, please click https://mitchcap.com/